Having good credit is an important part of your financial health. It can allow you to access the best quality credit products on the market. When you’re looking to take out a car loan or a mortgage, lenders look to your credit score when deciding to approve or decline your application.

Credit scores fluctuate according to your borrowing and repayment habits.

If you have had difficulty managing your finances in the past, missed payments or entered a debt relief program, like a consumer proposal or bankruptcy, your credit score will be negatively impacted.

With the right tools and resources, you can rebuild your credit. The important thing to keep in mind is that it takes time. Building credit is cumulative: it’s all about repeating positive behaviours and knowing which mistakes to avoid.

To rebuild your credit, the first step is making sure you understand how credit works. Every time you borrow money or apply for credit, the lenders send information about your account to the credit bureaus (Equifax and TransUnion), who then add the information to your credit report.

A credit report is a detailed report of your credit history, including a credit score and credit rating. It shows a summary of the amount and all types of credit you have, the length of time you have had these accounts, and your track record in paying bills. It is updated on a regular basis by companies that lend you money or issue credit cards (banks, credit unions, etc.).

Credit scores reflect a person’s borrowing habits, what they do or don’t do with the credit they have been given. A number of factors go into determining a credit score.

Payment history (35%)

Do you consistently make your payments on time? Your payment history is the most important component of your credit score. It includes all your past payment information, including payment deferrals, late and missed payments, collections and debt relief programs, like a consumer proposal or bankruptcy.

Amount owing (30%)

How much room do you have left on your existing debts? Having a balance of less than 30% of your credit limit is best, but if you have maxed out a credit card, lowering your balance by any amount will help improve your credit.

Length of credit history (15%)

The longer your credit history is, the more accurate your credit score will be in determining your borrowing habits.

New credit applications (10%)

How often do you apply for new credit? Credit agencies are notified every time a lender checks your credit following a credit application. So, avoid frequent “credit shopping,” which can lower your score.

Types of credit used (10%)

Having a credit history that includes different kinds of credit can reflect favourably on your credit score, like installment loans (car loans, personal loans), revolving credit (credit cards), or open credit (lines of credit).

Remember that your credit score can vary between financial institutions and credit bureaus. Other factors like your income, assets, the length of time at your current job can all be a part of a lender’s decision making process for assessing your risk level as a borrower.

Your credit score can vary between 300 to 900. The higher your credit score, the less risky you are in the eyes of lenders.

Your credit rating refers mainly to your credit history with a particular lender. Your credit rating is on a scale of 1 to 9, where the lower the number represents the better rating, with a letter that describes the type of credit:

I (for installment credit like car loan or bank loan);

O (open credit for line of credit or student loans);

R (revolving credit like a credit card).

Your credit score impacts your ability to get approved for new credit as well as the interest you will pay. The following chart demonstrates how your credit score influences interest rates, monthly payments and the total amount of interest you will pay over the course of a loan.

| Credit score: 675+ | Credit score: 551–674 | Credit score: 501–550 | Credit score: <500 | |

|---|---|---|---|---|

| Loan amount | $15,000 | $15,000 | $15,000 | $15,000 |

| Term (in months) | 60 | 60 | 60 | 60 |

| Interest rate | 6.9% | 9.9% | 15.9% | 29.9% |

| Monthly payment | $296 | $318 | $346 | $484 |

| Total paid | $17,760 | $19,080 | $20,760 | $29,040 |

| Total interest paid | $2,760 | $4,080 | $5,760 | $14,040 |

Both landlords and employers can sometimes request a copy of your credit report. A low credit score may prevent you from getting the apartment or job that you want.

You can request a copy of your report by phone, by mail or in person for free, with either Equifax or TransUnion. Many Canadian banks also provide your credit score for free through their websites.

It’s recommended that you review your credit report once a year to check for errors. If you find something that is incorrect, contact the credit reporting agency and your financial institution. You have the right to dispute any information on your credit report that you believe is wrong, and you can ask the credit bureaus to correct errors for free. Read more about checking for errors here.

A consumer proposal, debt management plan and bankruptcy all provide immediate debt relief and a path to an improved state of financial well-being, but they will affect your credit rating.

If you choose to file a consumer proposal or debt management plan, it will result in an R7 rating on your credit report, the second lowest rating that reporting agencies use. The consumer proposal will remain on your credit report for six years from the date of your filing or three years after you are discharged from the proposal, whichever comes first.

If you choose to file for bankruptcy, it will result in an R9 rating on your credit report, the lowest rating used by credit reporting agencies. The R9 rating stays on your report for six years after you’ve been discharged from bankruptcy.

But for many people, a debt forgiveness program can be the first step in improving their credit score. Debts that are overwhelming your finances will likely already be a strain on your credit. A debt relief program can help you establish new financial habits so you can better manage your finances. This will reflect positively on your credit score in the long term.

Starting to repair and rebuild your credit is an important goal for your long-term financial health. It’s a process that takes time. There are no quick fixes. Sound money management habits are the most important thing to remember when you’re trying to improve your credit score. A credit score has many different components because it’s a way of a assessing your overall financial health.

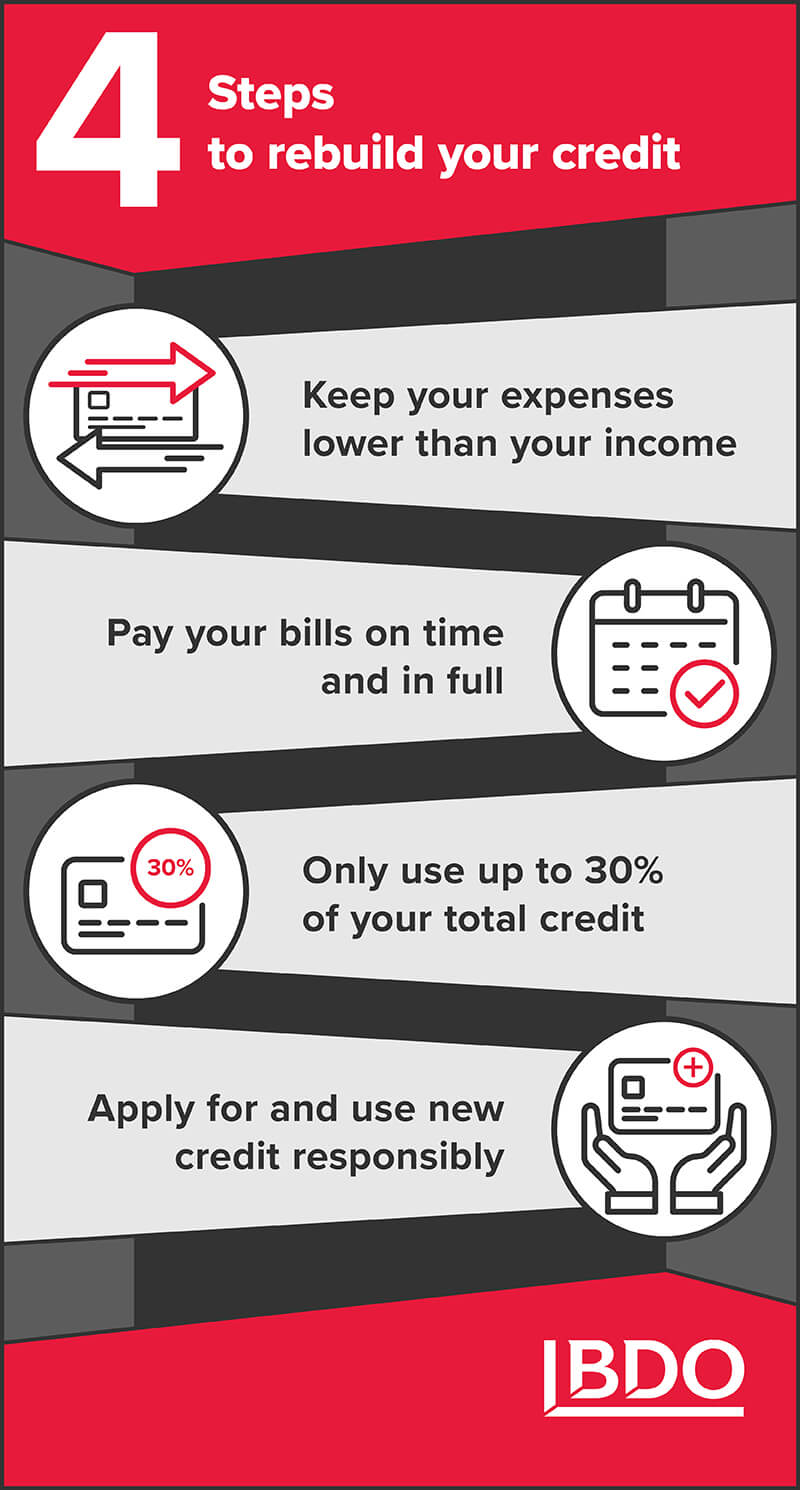

Learning how to budget so you can be mindful of your spending is the foundation of anyone’s financial health. How mindful are you of your money? How do you track your spending? Your credit score is a direct reflection of your financial health and your ability to manage your financial obligations.

It may seem like a late payment is not that serious but paying on time is part of your financial obligation towards your lender. When you pay in full and on time you are fulfilling the financial obligation and are proving that you are credit worthy.

Are your credit cards or lines of credit maxed out? Even lowering your balances to 75% of their limit will help. A 50% credit usage is very good, but 30% credit usage is excellent. Keeping your balances lower than your credit limit shows sound financial health and that you aren’t relying on credit to get by.

The more you use credit responsibly, the faster your credit score will improve. This means that you need to apply for new credit to improve your credit score. “Borrow, pay it off and repeat.” When lenders see that you have a history of paying off your debts, this lowers your risk profile.

There are companies that specialize in “credit repair services.” All they can do is help you fix errors in your credit bureau, which you can do yourself for free. The real improvement to a person’s credit score is in their future money management habits.

After budgeting, paying your bills on time and keeping your balances lower than their limits, what’s next?

The only way to prove to lenders that you have sound financial habits is to show them you can manage credit. If you adhere to the terms of a loan, by paying the loan off in full, your credit worthiness increases.

After a consumer proposal or bankruptcy, you will need to apply for a low-risk credit product, such as a secured credit card. A secured credit card requires you to deposit money upfront as security for the credit card.

A secured credit card is like any other credit card except you need to provide a cash deposit upfront. Learn how a secured credit card works.

Learn more