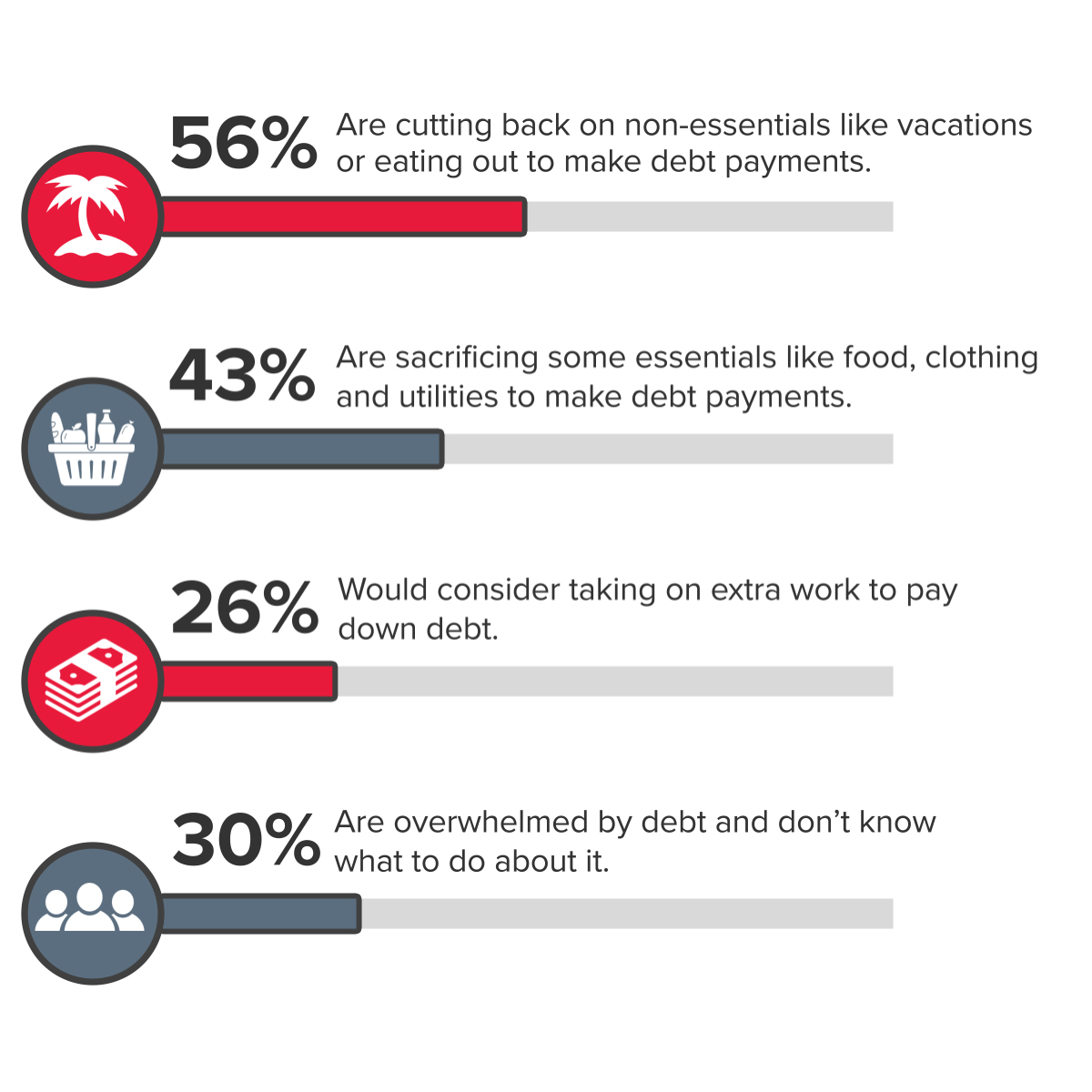

56% - are cutting back on non-essentials like vacations or eating out to make debt payments

43% - are sacrificing some essentials like food, clothing and utilities to make debt payments

26% - would consider taking on extra work to pay down debt

30% - are overwhelmed by debt and don’t know what to do about it